Electric Grid Reliability and Commercial Real Estate

Release Date: July 2026

This brief presents initial findings from Hickey Institute’s ongoing research into electric grid reliability and its implications for commercial real estate (CRE) development and investment. Drawing from previous research by Hickey Institute and public and private data sources, this brief synthesizes current market conditions, emerging challenges and strategic considerations facing CRE stakeholders.

Key findings include:

- Demand for electricity is surging due to rapid growth in power-intensive uses such as electric vehicle charging, AI data centers and cold storage facilities. At the same time, baseload power capacity is contracting due to the retirement of fossil fuel power plants.

- Commercial building owners can often pass rising utility costs on to tenants, but these costs can make buildings less competitive than those in less power-constrained markets.

- Texas, the Southwest and major data center corridors currently face the tightest energy markets and the greatest competition for available capacity, resulting in longer development timelines and higher installation costs than in other markets.

- Power availability is increasingly a key site selection determinant for occupiers, and power redundancy is a differentiator in markets where grid reliability is a concern. Buildings with features like backup power, energy-efficient design and renewable generation can often command rent premiums that justify related capital expenditures.

- Developers increasingly incorporate evaluations of local grid capacity and utility reliability into site selection. In markets where utility upgrades take years, some developers are willing to fund substation upgrades to accelerate project timelines.

- Addressing the challenges facing the grid will ultimately require federal and state policy solutions, but developers can partner with local officials and utility companies on capacity planning to better align infrastructure investments with development pipelines.

- The Crisis Reshaping CRE Investment

The CRE industry faces growing strains on energy infrastructure that are actively reshaping site selection, extending development timelines and threatening asset values across all property sectors. The U.S. electric grid, 70% of which is over 25 years old,1 is experiencing unprecedented demand growth as capacity contracts and reliability deteriorates. This collision is already disrupting CRE, forcing developers to reconsider projects in power-constrained markets and compelling investors to reconsider risk across portfolios.

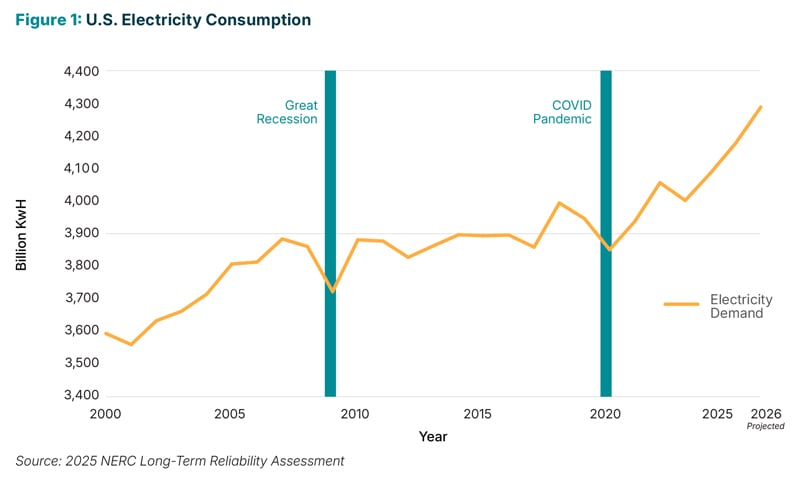

According to North American Electric Reliability Corporation (NERC)’s 2025 Long-Term Reliability Assessment, summer peak demand is forecast to grow by 224 gigawatts (GW) over the next decade, a more than 69% increase over the previous year’s forecast. Winter peak demand is projected to rise by 246 GW over the same period. Thirteen of 23 assessment areas now face elevated or high resource adequacy risks, with high-risk regions including those managed by the Midcontinent Independent System Operator, PJM and Electric Reliability Council of Texas grid operators.2 In high-growth markets, utilities report demand surging 10% to 20% annually, a pace that infrastructure cannot match when new transmission takes seven to 10 years to permit and build.3 Equipment lead times have doubled, with transformers requiring 12 to 18 months for delivery.4 Developers once treated connecting to the grid as administrative coordination, but it has increasingly become a critical path determining whether projects proceed at all.

For developers and investors, the strategic implications are profound. Markets that were attractive six months ago can be at capacity before developers complete due diligence. Sites that were viable during initial evaluation are subsequently rejected by utilities that prove unable to commit to service timelines. Prospective industrial tenants walk away when a building’s power reliability becomes uncertain. Office landlords field tenant requirements for energy resilience features that were uncommon two years ago. The question is no longer whether to factor grid constraints into development and investment decisions, but whether companies can adapt to these constraints before their competitors do.

Understanding the Demand Surge

Three forces are driving growth in electricity demand at rates not seen since the mid-20th century. First, artificial intelligence computing is fundamentally changing data center power consumption. A single ChatGPT query requires 10 times the electricity of a Google search. The Electric Power Research Institute projects data centers could consume up to 9% of U.S. electricity generation by 2030, more than double current levels.5 Although data centers are the most power-intensive form of new commercial development, their growth is also reshaping utility capacity allocation across all commercial users.

In markets like Northern Virginia, Phoenix, and Dallas-Fort Worth, utilities are navigating how to balance priorities between large power users and traditional commercial development. Developers pursuing office or industrial projects discover that capacity identified during site searches has been reallocated. As data centers consume a growing share of new generation, other commercial users face longer wait times, higher infrastructure costs and sometimes outright unavailability. The competition for electrons has become as important as competition for entitled land.

Second, electric vehicle infrastructure carries implications that extend far beyond transportation. EV registrations grew from fewer than 100,000 in 2012 to over 3 million by 2022, with projections reaching up to 34 million by 2030, although recent policy changes may moderate this trajectory. Office landlords face tenant requirements for EV charging that can substantially increase a building’s electrical load, with large deployments requiring significant upgrades to power supply and distribution infrastructure.6 Multifamily developers must decide whether to oversize electrical service substantially beyond immediate needs (expensive when construction costs remain elevated) or risk property obsolescence as EV adoption accelerates. Industrial facilities planning electric delivery fleets face steeper challenges. DC (direct current) fast charging can double or triple power requirements, triggering utility demands for load studies, transformer upgrades or substation improvements at the developer’s expense.

Third, temperature-controlled logistics has expanded rapidly. Online grocery sales increased 54% in 2021, driving unprecedented demand for refrigerated warehousing. Cold storage facilities use approximately 25 kilowatt-hours per square foot annually just for cooling, a figure that is substantially higher in warm climates where systems run continuously. These facilities are becoming among the most power-intensive industrial users, competing with manufacturing and data centers for limited capacity. Cold storage projects that would have been routine five years ago now require extensive utility coordination and infrastructure investment previously reserved for heavy industrial users.7

The Supply Crisis: When Infrastructure Cannot Keep Pace

Even as demand accelerates, traditional baseload power capacity is contracting. Nearly two-thirds of fossil fuel-fired generation capacity is expected to reach end of life by 2035.8 While renewable deployment has accelerated, wind and solar are inherently variable, and energy storage is only beginning to deploy at utility scale. For developers, this creates a critical distinction: A site’s power availability is not just about nameplate capacity but also whether that capacity is firm and dispatchable or intermittent and weather-dependent.

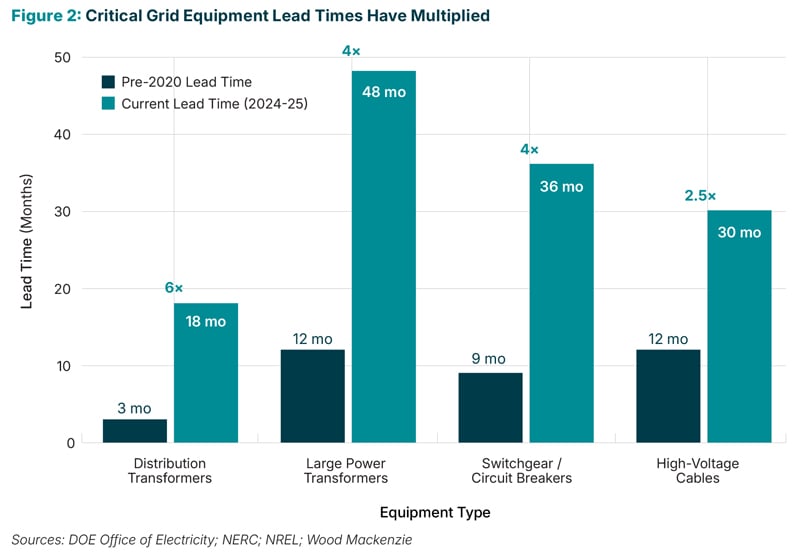

Supply chain constraints compound the problem. Lead times for critical power equipment have nearly doubled. Transformers and switchgear face delivery schedules of 12 to 18 months, up from six months historically. These delays cascade into project timelines. Developers securing site control and entitlements discover utility service connection dates have become the critical path item, pushing building delivery by quarters or years. This uncertainty complicates pre-leasing and financial modeling, as tenants hesitate to commit when power availability dates remain uncertain.

Texas provides a cautionary tale for the stability of the electric grid. A February 2021 winter storm left millions without power for days, resulting in 246 deaths9 and exposing systemic vulnerabilities. Despite the state’s booming economy and business-friendly environment, tenants, particularly those in data-intensive industries, increasingly demand detailed information about backup power capabilities. Industrial users evaluating Texas sites are budgeting for more robust on-site generation and microgrid capabilities, adding materially to infrastructure costs. These are prerequisite investments to mitigate grid reliability risk that did not exist a decade ago.

Rising Power Costs: The Hidden Threat to Operating Performance

Beyond availability concerns, rising electricity costs threaten operating performance and valuations. As utilities invest billions in grid modernization, these costs are passed through to ratepayers. U.S. Energy Information Administration data reveal dramatic regional variation, with increases from February 2025 to February 2026 ranging from modest single digits in many states to over 20% in Ohio and Virginia.10 Prices have since grown more volatile due to conflict in the Middle East.

For investors, these trajectories introduce cash flow pressure and valuation risk. Commercial buildings with net leases may pass costs through to tenants, but rising energy expenses often make these properties harder to lease. Energy costs have a particularly large impact on an industrial building’s competitiveness, as manufacturers evaluate total occupancy expenses. Multifamily operators face direct margin compression as utility costs rise faster than rent growth. A seemingly modest 5% to 7% annual increase compounds to 40% to 50% over a typical 10-year hold period, materially affecting net operating income projections.

The challenge extends beyond historical trends to future trajectories. Thirty-five states and Washington, D.C., have renewable portfolio standards or clean energy goals requiring 50% to 100% renewable electricity by 2040 to 2050.11 Achieving these targets requires massive infrastructure investment, including new transmission, energy storage and grid modernization, all recovered through utility rates. Markets that have been aggressive in renewable adoption are already experiencing rate impacts. Markets beginning the transition face steeper future increases. Community reaction adds complexity, as resident concerns about energy requirements for new development create opposition that can delay or derail otherwise viable projects.

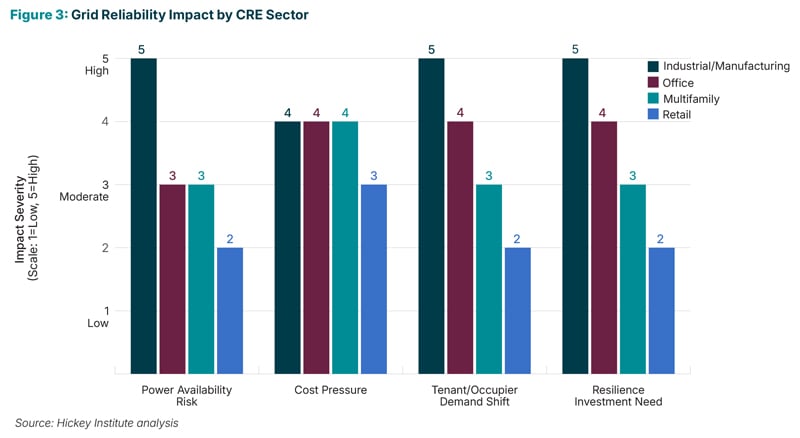

Regional Pressure Points and Sector-Specific Implications

Where Grid Constraints Hit Hardest

Texas currently represents the most acute case despite strong fundamentals. The state’s isolated grid creates unique exposure to supply-demand imbalances. Beyond the 2021 winter storm disaster, Texas faces chronic summer capacity challenges. The state’s traditional advantages (no state income tax, business-friendly regulations, abundant land) are now counterbalanced by grid reliability questions. Industrial users are building in expensive redundancy features that erode Texas’ cost advantage. Office landlords invest in backup power to remain competitive. Even multifamily developers incorporate resilience features, adding to construction costs.

The Southwest heat belt (Arizona, Nevada, Southern California) faces parallel challenges from extreme cooling loads during intense heat events. Arizona utilities are investing aggressively in battery storage, with Salt River Project recently commissioning a 1 gigawatt-hour system.12 Nevertheless, investments still lag in the race to keep pace with data center construction, semiconductor manufacturing and population growth. Before approving service connections, Phoenix and Las Vegas utilities now request demand management plans requiring large users to reduce consumption during peak periods or grid emergencies. Industrial projects that would have been able to secure utility commitments in 90 to 120 days in earlier years now face nine- to 12-month processes, if not longer. Properties that functioned adequately five years ago require expensive retrofits to remain competitive.

Data center corridors (Northern Virginia, Dallas, Phoenix) face challenges driven by their own success. Dominion Energy in Northern Virginia has announced multibillion-dollar upgrades,13 but developers report connection wait times stretching years for large loads, including manufacturing facilities requiring 10-plus megawatts, large cold storage operations, and mixed-use developments with substantial EV charging infrastructure. Similar dynamics emerge in Dallas and Phoenix as data center development collides with residential growth and industrial expansion. Competition for capacity forces developers across property types to accept extended timelines, fund infrastructure upgrades or look to secondary markets at higher overall costs.

Industrial and Manufacturing

For industrial developers, power availability has elevated to become a primary site selection determinant. Companies request utility commitment letters earlier and walk away when service timelines prove uncertain. Site selectors report that clients explicitly ask about grid capacity, renewable power availability and utility reliability before shortlisting markets. Developers front-load utility engagement, conduct due diligence before securing site control, and in constrained markets invest in infrastructure that is traditionally the utility’s responsibility, such as substation expansions, transformer installations and distribution upgrades. Some build redundancy from the start, including backup generators for full loads, microgrid capabilities and on-site solar-plus-storage. These add 10% to 20% to infrastructure costs but are increasingly competitive necessities.

Advanced manufacturing presents acute challenges. Semiconductor fabrication and pharmaceutical production require uninterrupted power, with voltage quality exceeding standard service. Millisecond fluctuations can ruin production runs, causing millions in losses. These users treat power infrastructure as a first-order location determinant. Markets demonstrating available capacity and proven reliability with redundant feeds and minimal disruptions capture disproportionate investment. Those unable to demonstrate reliability are excluded regardless of other advantages.

Office and Multifamily

Office properties are faced with tenant demands for building resilience and the realities of energy performance reshaping competitive positioning. Properties with robust backup power that covers more than life-safety loads, modern building management systems, and demonstrated efficiency command measurable rent premiums and achieve higher occupancy.

CBRE research across more than 20,600 office buildings found LEED-certified properties command an average 4% rent premium over comparable non-certified buildings. The firm’s 2024 Americas Office Occupier Sentiment Survey found 21% of corporate occupiers would pay a premium for certified space while 18% would reject non-certified options outright.14

Corporate occupiers increasingly require buildings that demonstrate both environmental responsibility through renewable energy and operational reliability through backup systems. Properties delivering both (through on-site solar, battery storage and grid-interactive capabilities) capture the most credit-worthy tenants and longest lease terms. These dynamics are most pronounced in primary markets with institutional ownership and credit tenants; developers in secondary markets report more mixed willingness by tenants to pay for sustainability and resilience features.

Multifamily developers face complex infrastructure planning. Many residents expect EV charging, but timing is uncertain. Installing charging at scale requires oversizing electrical service substantially beyond immediate needs. For a 300-unit project, planning for 50 to 75 charging stations might require 25% to 40% more capacity, representing hundreds of thousands in additional costs. Yet not planning adequately for charging risks obsolescence within typical hold periods.

Properties in markets prone to disruptions face additional pressures. Buildings experiencing occasional outages see negative reviews and retention challenges. Properties compete on reliability features, including backup generators for common areas, battery backup options and building-wide microgrid capabilities. These features are evolving from luxury differentiators to baseline expectations.

Strategic Responses and The Business Case

Developers in some markets should consider making fundamental changes to adapt to current conditions. The practices described below are most prevalent in power-constrained markets including Texas, the Southwest and data center corridors, although adoption is spreading to other high-growth regions as grid challenges intensify.

The most critical practice is to shift utility engagement from late-stage execution to early-stage due diligence. In the authors’ recent experience, developers are conducting utility due diligence before securing site control, having preliminary discussions during site search and walking away when capacity timelines prove uncertain. Purchase agreements increasingly include contingencies tied to utility capacity commitments with specific timelines. Developers are extending feasibility periods to accommodate six to 12 months of utility coordination. Those with existing utility relationships and track records win deals over competitors offering higher prices, reflecting how critical capacity has become.

Site selection criteria must evolve. Developers and investors continue to evaluate locations based on labor, logistics and incentives, but grid capacity, utility reliability, infrastructure investment plans and regulatory approaches must now carry equal weight. Sophisticated developers build utility assessment into market screening, eliminating regions without credible paths to required capacity before analyzing other factors. Power availability now operates as a go/no-go threshold. A market scoring highly on traditional metrics but unable to demonstrate available, reliable power is not viable.

Infrastructure co-investment models are emerging as strategic responses. Rather than waiting for utility upgrades that might take years, some developers are funding substation expansions, transformer installations or distribution extensions themselves to accelerate timelines and secure otherwise unavailable capacity. A developer funding a $3 million to $5 million substation upgrade for a $200 million project may appear to absorb utility costs inappropriately, but when the alternative is a two-year delay potentially causing the loss of a committed lease, the infrastructure investment becomes the least expensive option.

Microgrid development has shifted from an exotic option to mainstream consideration. These localized energy systems typically combine multiple generation and storage components (most commonly solar arrays, battery storage systems and backup generators, with some incorporating fuel cells or small gas turbines) that can operate independently from the main grid during outages. Localized systems operating independently provide resilience and reduced dependence on constrained utilities. The economic case improves as reliability degrades and technology costs decline. While up-front capital remains substantial, often $2,000 to $3,000 per kilowatt,15 the value proposition accounts for avoided downtime, tenant retention benefits and potential rent premiums. It is worth noting that traditional CRE lenders do not typically underwrite microgrid investments, requiring developers to pursue alternative financing structures or self-fund these improvements.

Portfolio risk assessment is essential for multi-asset owners, who increasingly evaluate facilities for concentrated grid vulnerability: Do multiple assets depend on the same utility territory? Are properties concentrated in markets with reliability challenges? Smart diversification involves identifying risk correlations and deliberately building portfolios that reduce them.

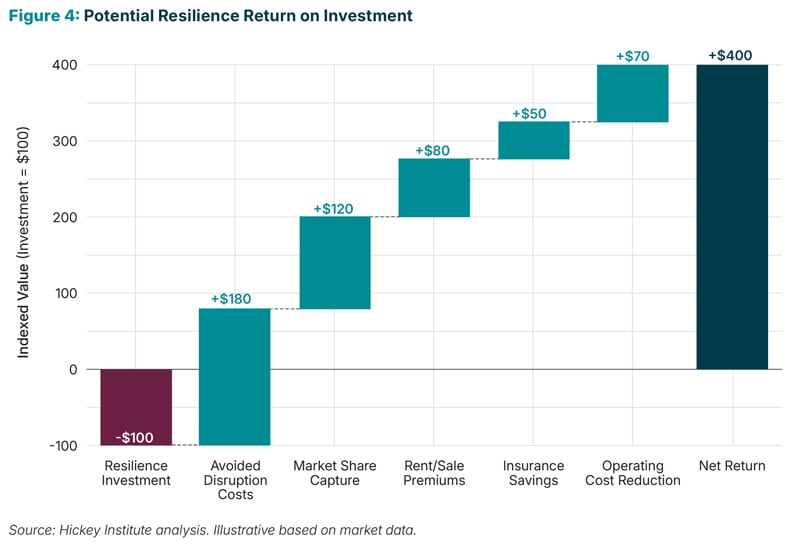

Quantifying Resilience Returns

Resilience investments often face scrutiny, being viewed as defensive costs rather than value-creating strategies. However, evidence demonstrates properly structured resilience generates returns that can significantly exceed costs. The most direct return comes from avoided disruption costs. A facility losing $5 million annually to disruptions, if reduced 60% through resilience, saves $3 million per year, worth more than $40 million present value over 20 years at typical discount rates.

Beyond avoided losses, resilience allows occupiers to capture market share during competitor disruptions. When Hurricane Harvey struck Houston in 2017, facilities with backup power maintained operations, while competitors shut down for weeks. Companies captured displaced customer demand that became permanent market share gains. Revenue protection alone exceeded resilience costs by eight to 12 times. Similar dynamics occurred during the 2021 Texas freeze and California wildfires.

Valuation impacts provide additional returns. Industrial properties with reliability infrastructure can command measurable rent and sale premiums, with the spread most pronounced in power-constrained markets. Office buildings with resilience features often achieve higher occupancy and premium rents.

Operating cost reductions can create ongoing value: Insurance premiums decline 10% to 25%,16 energy costs decrease through efficiency improvements, and maintenance costs drop. The total return (avoided losses, market share protection, property premiums, insurance reductions, operating savings, enhanced retention) can exceed resilience costs by five times over a typical 10- to 15-year institutional holding period. Returns accrue primarily to owners through property value appreciation and reduced operating costs, while occupiers benefit from business continuity and operational savings.

Looking Forward: The Window for Strategic Advantage

The CRE industry is at an inflection point. Grid reliability challenges that seemed abstract three years ago are now actively reshaping development economics, investment strategies and competitive positioning. Stakeholders who recognize this reality and adapt are capturing advantages that will compound for years. Those treating power as an afterthought accumulate risks manifesting in extended timelines, cost overruns, tenant losses and diminished asset values.

Several strategic imperatives emerge. First, proactive developers are conducting rigorous and early-stage power due diligence alongside market analysis and entitlement feasibility. This process includes building relationships with utility planners, understanding grid operators’ capacity forecasts, tracking infrastructure investment programs and evaluating sites for credible paths to future requirements.

Second, developers are increasingly incorporating energy resiliency into building design. The next generation of competitive properties will feature backup power sized for actual operations, advanced building management systems responding to grid conditions in real time, renewable generation assets reducing grid dependence and, where appropriate, microgrid infrastructure enabling energy independence. These require up-front capital but can generate returns through multiple channels.

Third, investors are increasingly addressing grid risk concentration and diversification in their portfolio strategies by mapping existing holdings against grid reliability risks and identifying concentrations that create correlated vulnerabilities. A REIT with substantial Texas exposure faces different risk profiles than one diversified across multiple grid regions. Strategic portfolio management means deliberately diversifying across uncorrelated risk dimensions (geography, utility providers, grid operators) to reduce total vulnerability even if individual site costs increase modestly.

Fourth, effectively addressing the challenges that face the grid will require policy solutions. The multiyear delays now common in interconnection queues add cost and uncertainty that ripple through project timelines. Expedited processes to connect to the grid could help, but expansion of transmission remains the longer-term answer to regional capacity constraints. Unlocking that investment will require regulatory frameworks that make public-private partnerships viable. At the local level, economic development officials and the CRE industry can partner with utilities on capacity planning to better align infrastructure investment with development pipelines.

The window for strategic advantage remains open but is narrowing. As grid challenges intensify, resilience will shift from differentiator to prerequisite. Markets that solve power availability will capture disproportionate investment, and developers who master utility coordination will win deals others cannot execute. Properties with genuine resilience features will separate from commodity buildings on both rent and price. The advantage belongs to those acting now while competitors are still figuring out that the rules have changed.

About the Commercial Real Estate Development Association

The Commercial Real Estate Development Association (CREDA) is the leading global professional organization for the commercial real estate industry, representing more than 21,000 members across 55 chapters in North America. CREDA equips professionals with the resources, relationships and insights needed to advance their careers through high-impact networking, practical education and forward-looking research. As a trusted voice at the forefront of the industry, CREDA drives innovation in development by advocating for legislation that supports commercial real estate growth and delivering data-driven insights through the CREDA Research Foundation.

The Commercial Real Estate Development Association Research Foundation was established in 2000 as a 501(c)(3) organization to advance the knowledge of the commercial real estate development industry through objective research, analysis and education. By delivering data-driven insights on the industry’s economic impacts and market dynamics, the Foundation equips industry leaders, policymakers and stakeholders with information they need to make informed decisions and create thriving communities. For more information, visit credaresearch.foundation.

About Hickey Institute

The Hickey Institute produces independent research and commentary on where companies invest, expand, and build, and why. By examining the policies, economics, and strategies behind location decisions, from incentives and federal policy to labor markets, supply chains, and risk, the Institute covers terrain that rarely gets examined on all three terms at once. Founded as a joint effort of Hickey & Associates, the global site selection and incentives advisory firm, and Hickey Global, the economic development consulting firm, the Institute brings the corporate and community sides of every location decision into the same conversation.

Disclaimer

This project is intended to provide information and insights to industry practitioners and does not constitute advice or recommendations. The CREDA Research Foundation disclaims any liability for actions taken because of this project and its findings.

© 2026 Commercial Real Estate Development Association Research Foundation

There are many ways to give to the Foundation and support projects and initiatives that advance the commercial real estate industry. If you would like to contribute to the Foundation, please contact Christopher Ware, vice president of partnerships and strategic initiatives, CREDA, at 703-674-1419 or cware@credaglobal.org.

For information about the Foundation’s research, please contact Shawn Moura, Ph.D, executive director of the CREDA Research Foundation, at 703-904-7100, ext. 117, or smoura@credaglobal.org.

Endnotes

1 Hickey & Associates, “Running Out of Power,” Hickey Institute, 2024, https://www.hickeyandassociates.com/runningoutofpowerreport.

2 North American Electric Reliability Corporation, “2025 Long-Term Reliability Assessment,” January 2026, https://www.nerc.com/pa/APA/ra/Pages/default.aspx.

3 U.S. Department of Energy, “National Transmission Needs Study,” October 2023, https://www.energy.gov/gdo/national-transmission-needs-study.

4 U.S. Department of Energy, Office of Electricity, “DOE and Industry Team Up to Keep the Lights on for America,” February 22, 2024, https://www.energy.gov/oe/articles/doe-and-industry-team-keep-lights-america.

5 Electric Power Research Institute, “Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption,” May 28, 2024, https://www.epri.com/research/products/000000003002028905.

6 Zealan Hoover et al., “How Charging in Buildings Can Power Up the Electric-Vehicle Industry,” McKinsey & Company, January 5, 2021, https://www.mckinsey.com/industries/electric-power-and-natural-gas/our-insights/how-charging-in-buildings-can-power-up-the-electric-vehicle-industry.

7 Hickey & Associates, “Running Out.”

8 Ibid.

9 Texas Department of State Health Services, “February 2021 Winter Storm-Related Deaths–Texas,” December 31, 2021, https://www.dshs.texas.gov/sites/default/files/news/updates/SMOC_FebWinterStorm_MortalitySurvReport_12-30-21.pdf.

10 U.S. Energy Information Administration, “Electric Power Monthly,” Table 5.6.a, Average Retail Price of Electricity, April 23, 2026, https://www.eia.gov/electricity/monthly/.

11 National Conference of State Legislatures, “State Renewable Portfolio Standards and Goals,” August 13, 2021, https://www.ncsl.org/energy/state-renewable-portfolio-standards-and-goals.

12 Salt River Project, “Arizona’s Largest Battery is Now Operating on SRP’s Power Grid,” news release, March 14, 2024, https://media.srpnet.com/arizonas-largest-battery-is-now-operating-on-srps-power-grid-supporting-google-along-with-otherclean-energy-resources/.

13 Dominion Energy Virginia, “2024 Integrated Resource Plan,” October 15, 2024, https://www.dominionenergy.com/about/our-company/irp. Dominion has announced $50.1 billion in capital projects between 2025 and 2029, including transmission, distribution and generation resources.

14 CBRE, “Green is Good: The Enduring Rent Premium of LEED-Certified U.S. Office Buildings,” October 26, 2022, https://www.cbre.com/insights/viewpoints/green-is-good-the-endurance-of-the-rent-premium-in-leed-certified-us-office-buildings; CBRE, “2024 Americas Office Occupier Sentiment Survey,” August 13, 2024, https://www.cbre.com/insights/reports/2024-americas-office-occupier- sentiment-survey.

15 Hickey & Associates, “Running Out.”

16 FM Global, “FM Property Loss Prevention Data Sheets,” https://fm.com/datasheets. Premium reductions vary by property type, location and scope of resilience improvements.